Credit Risk Assessment

Loans form an integral part of banking operations. However, not all the loans are promptly returned and hence it is important for a bank to closely monitor its loan applications. This project is an analysis of the German credit dataset from the UCI Machine Learning repository. The dataset contains details of 1000 loan applicants with 21 attributes along with the classification as good or bad credit.

In this project, the relationship between the credit risk and various attributes will be explored through basic statistical techniques and presented through visualizations.

Contents

- Import data

- Data preparation, cleaning

- Exploratory data analysis

- Feature engineering

- Models

- Model evaluation

- Conclusion

- References

1. Import data

Let’s begin by downloading the data from the UCI Machine Learning repository.

from urllib.request import urlretrieve

urlretrieve('http://archive.ics.uci.edu/ml/machine-learning-databases/statlog/german/german.data', 'german.data')

('german.data', <http.client.HTTPMessage at 0x7effdfbb5550>)

The dataset has been downloaded and extracted.

2. Data Preparation and Cleaning

In this step, we do data preparation and cleaning, making the data suitable for subsequent analysis.

2.1 Load data into dataframe

The datafile is in .data format, delimited with space, and has no headers.

import pandas as pd

german_df = pd.read_csv('http://archive.ics.uci.edu/ml/machine-learning-databases/statlog/german/german.data',

delimiter=' ',header=None)

Now, let’s have an overview of the dataset.

german_df.info()

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 1000 entries, 0 to 999

Data columns (total 21 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 0 1000 non-null object

1 1 1000 non-null int64

2 2 1000 non-null object

3 3 1000 non-null object

4 4 1000 non-null int64

5 5 1000 non-null object

6 6 1000 non-null object

7 7 1000 non-null int64

8 8 1000 non-null object

9 9 1000 non-null object

10 10 1000 non-null int64

11 11 1000 non-null object

12 12 1000 non-null int64

13 13 1000 non-null object

14 14 1000 non-null object

15 15 1000 non-null int64

16 16 1000 non-null object

17 17 1000 non-null int64

18 18 1000 non-null object

19 19 1000 non-null object

20 20 1000 non-null int64

dtypes: int64(8), object(13)

memory usage: 164.2+ KB

The dataset contains 21 variables and 1000 observations. 8 variables are of numeric type and 13 of object type. As the object type variables do not have any null values, we can conclude that they are of categorical type.

2.2 Label the columns

Next, let’s label the variables for ease of use. The document describing the dataset may be referred for this.

urlretrieve('http://archive.ics.uci.edu/ml/machine-learning-databases/statlog/german/german.doc', 'german.doc')

f = open('german.doc')

german_doc= f.read()

print(german_doc)

Description of the German credit dataset.

1. Title: German Credit data

2. Source Information

Professor Dr. Hans Hofmann

Institut f"ur Statistik und "Okonometrie

Universit"at Hamburg

FB Wirtschaftswissenschaften

Von-Melle-Park 5

2000 Hamburg 13

3. Number of Instances: 1000

Two datasets are provided. the original dataset, in the form provided

by Prof. Hofmann, contains categorical/symbolic attributes and

is in the file "german.data".

For algorithms that need numerical attributes, Strathclyde University

produced the file "german.data-numeric". This file has been edited

and several indicator variables added to make it suitable for

algorithms which cannot cope with categorical variables. Several

attributes that are ordered categorical (such as attribute 17) have

been coded as an integer. This was the form used by StatLog.

6. Number of Attributes german: 20 (7 numerical, 13 categorical)

Number of Attributes german.numer: 24 (24 numerical)

7. Attribute description for german

Attribute 1: (qualitative)

Status of existing checking account

A11 : ... < 0 DM

A12 : 0 <= ... < 200 DM

A13 : ... >= 200 DM /

salary assignments for at least 1 year

A14 : no checking account

Attribute 2: (numerical)

Duration in month

Attribute 3: (qualitative)

Credit history

A30 : no credits taken/

all credits paid back duly

A31 : all credits at this bank paid back duly

A32 : existing credits paid back duly till now

A33 : delay in paying off in the past

A34 : critical account/

other credits existing (not at this bank)

Attribute 4: (qualitative)

Purpose

A40 : car (new)

A41 : car (used)

A42 : furniture/equipment

A43 : radio/television

A44 : domestic appliances

A45 : repairs

A46 : education

A47 : (vacation - does not exist?)

A48 : retraining

A49 : business

A410 : others

Attribute 5: (numerical)

Credit amount

Attribute 6: (qualitative)

Savings account/bonds

A61 : ... < 100 DM

A62 : 100 <= ... < 500 DM

A63 : 500 <= ... < 1000 DM

A64 : .. >= 1000 DM

A65 : unknown/ no savings account

Attribute 7: (qualitative)

Present employment since

A71 : unemployed

A72 : ... < 1 year

A73 : 1 <= ... < 4 years

A74 : 4 <= ... < 7 years

A75 : .. >= 7 years

Attribute 8: (numerical)

Installment rate in percentage of disposable income

Attribute 9: (qualitative)

Personal status and sex

A91 : male : divorced/separated

A92 : female : divorced/separated/married

A93 : male : single

A94 : male : married/widowed

A95 : female : single

Attribute 10: (qualitative)

Other debtors / guarantors

A101 : none

A102 : co-applicant

A103 : guarantor

Attribute 11: (numerical)

Present residence since

Attribute 12: (qualitative)

Property

A121 : real estate

A122 : if not A121 : building society savings agreement/

life insurance

A123 : if not A121/A122 : car or other, not in attribute 6

A124 : unknown / no property

Attribute 13: (numerical)

Age in years

Attribute 14: (qualitative)

Other installment plans

A141 : bank

A142 : stores

A143 : none

Attribute 15: (qualitative)

Housing

A151 : rent

A152 : own

A153 : for free

Attribute 16: (numerical)

Number of existing credits at this bank

Attribute 17: (qualitative)

Job

A171 : unemployed/ unskilled - non-resident

A172 : unskilled - resident

A173 : skilled employee / official

A174 : management/ self-employed/

highly qualified employee/ officer

Attribute 18: (numerical)

Number of people being liable to provide maintenance for

Attribute 19: (qualitative)

Telephone

A191 : none

A192 : yes, registered under the customers name

Attribute 20: (qualitative)

foreign worker

A201 : yes

A202 : no

8. Cost Matrix

This dataset requires use of a cost matrix (see below)

1 2

----------------------------

1 0 1

-----------------------

2 5 0

(1 = Good, 2 = Bad)

the rows represent the actual classification and the columns

the predicted classification.

It is worse to class a customer as good when they are bad (5),

than it is to class a customer as bad when they are good (1).

Based on the description, we name the columns.

german_df.columns=['account_bal','duration','payment_status','purpose',

'credit_amount','savings_bond_value','employed_since',

'intallment_rate','sex_marital','guarantor','residence_since',

'most_valuable_asset','age','concurrent_credits','type_of_housing',

'number_of_existcr','job','number_of_dependents','telephon',

'foreign','target']

german_df= german_df.replace(['A11','A12','A13','A14', 'A171','A172','A173','A174','A121','A122','A123','A124'],['neg_bal','positive_bal','positive_bal','no_acc','unskilled','unskilled','skilled','highly_skilled',

'none','car','life_insurance','real_estate'])

3. Exploratory Data Analysis and Visualization

# import libraries for visualizations

import numpy as np

import seaborn as sns

import matplotlib

import matplotlib.pyplot as plt

%matplotlib inline

sns.set_style('darkgrid')

matplotlib.rcParams['font.size'] = 14

matplotlib.rcParams['figure.figsize'] = (9, 5)

matplotlib.rcParams['figure.facecolor'] = '#00000000'

3.1 Examine missing values

# check for missing values

german_df.isna().any().any()

False

3.1 Examine distribution of target column

german_df.target.unique()

array([1, 2])

The target column has two values:

- 1: representing a good loan

- 2: representing a bad (defaulted) loan.

The usual convention is to use ‘1’ for bad loans and ‘0’ for good loans. Let’s replace the values to comply to the convention.

from sklearn.preprocessing import LabelEncoder

le= LabelEncoder()

le.fit(german_df.target)

german_df.target=le.transform(german_df.target)

german_df.target.head(5)

0 0

1 1

2 0

3 0

4 1

Name: target, dtype: int64

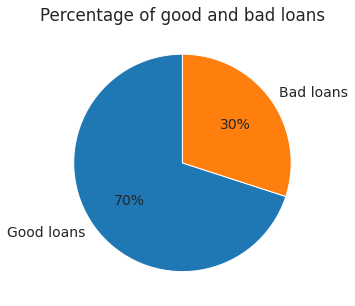

An understanding of the percentage of good and bad loans would be useful for further analysis. A pie chart would be the best tool to help with this.

good_bad_per=round(((german_df.target.value_counts()/german_df.target.count())*100))

good_bad_per

plt.pie(good_bad_per,labels=['Good loans', 'Bad loans'], autopct='%1.0f%%', startangle=90)

plt.title('Percentage of good and bad loans');

The pie chart shows that 30% of the loan applicants defaulted. From this information, we see that this is an imbalanced class problem. Hence, we will have to weigh the classes by their representation in the data to reflect this imbalance.

4.2 Exploration of continues variables

- Summary statistics

- Histograms

- Box-plots

Observations

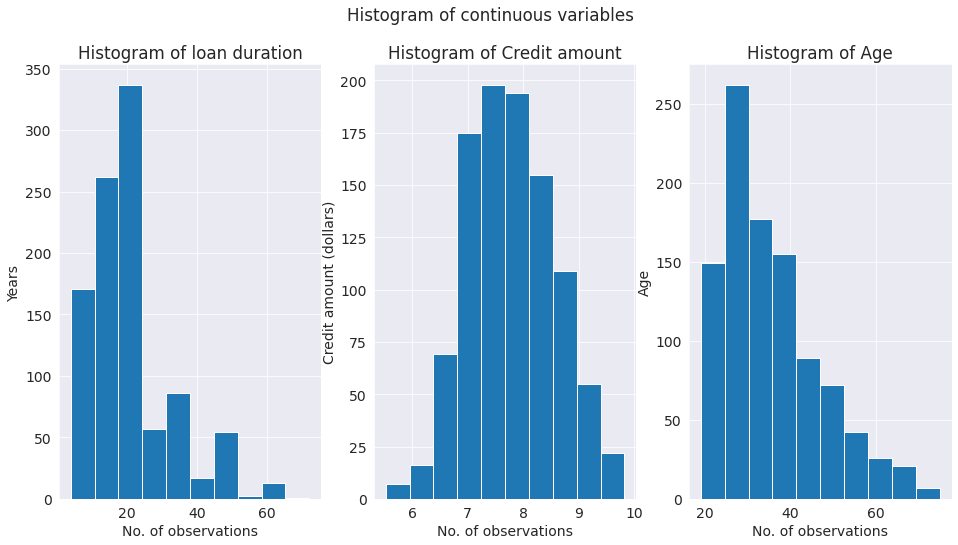

- A glance of the distribution of the continues variables shows that there is a wide gap in the range of variables. The credit amount variable might have to be transformed to bring all variables to similar range.

- The histogram suggests that the credit amount is approximately normally distributed. However, age and duration have a skewed distribution.

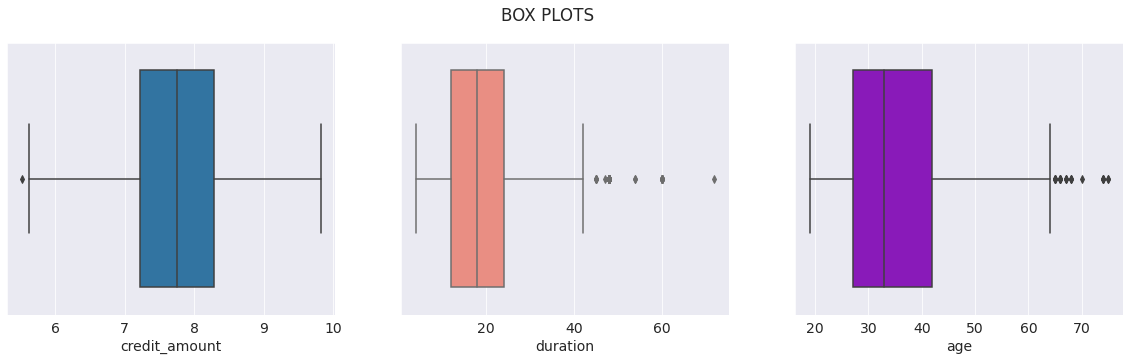

- The box plots show that most of the credits amounts are between 1000 to 4500 dollars. The credit amount is positively skewed. Most of the loan duration is from 15 to 30 months. Majority of the loan applicants have age between 28 - 43.

german_df[['credit_amount','duration','age']].describe()

| credit_amount | duration | age | |

|---|---|---|---|

| count | 1000.000000 | 1000.000000 | 1000.000000 |

| mean | 3271.258000 | 20.903000 | 35.546000 |

| std | 2822.736876 | 12.058814 | 11.375469 |

| min | 250.000000 | 4.000000 | 19.000000 |

| 25% | 1365.500000 | 12.000000 | 27.000000 |

| 50% | 2319.500000 | 18.000000 | 33.000000 |

| 75% | 3972.250000 | 24.000000 | 42.000000 |

| max | 18424.000000 | 72.000000 | 75.000000 |

german_df['credit_amount']=np.log(german_df['credit_amount'])

german_df[['credit_amount','duration','age']].describe()

| credit_amount | duration | age | |

|---|---|---|---|

| count | 1000.000000 | 1000.000000 | 1000.000000 |

| mean | 7.788691 | 20.903000 | 35.546000 |

| std | 0.776474 | 12.058814 | 11.375469 |

| min | 5.521461 | 4.000000 | 19.000000 |

| 25% | 7.219276 | 12.000000 | 27.000000 |

| 50% | 7.749107 | 18.000000 | 33.000000 |

| 75% | 8.287088 | 24.000000 | 42.000000 |

| max | 9.821409 | 72.000000 | 75.000000 |

# histograms of continues variables

fig, axes = plt.subplots(1,3, figsize=(16,8))

plt.suptitle('Histogram of continuous variables')

axes[0].hist(german_df['duration'])

axes[0].set_xlabel('No. of observations')

axes[0].set_ylabel('Years')

axes[0].set_title('Histogram of loan duration');

axes[1].hist(german_df['credit_amount'])

axes[1].set_xlabel('No. of observations')

axes[1].set_ylabel('Credit amount (dollars)')

axes[1].set_title('Histogram of Credit amount');

axes[2].hist(german_df['age'])

axes[2].set_xlabel('No. of observations')

axes[2].set_ylabel('Age')

axes[2].set_title('Histogram of Age');

# box-plots of continues variables

fig, ax = plt.subplots(1,3,figsize=(20,5))

plt.suptitle('BOX PLOTS')

sns.boxplot(german_df['credit_amount'], ax=ax[0]);

sns.boxplot(german_df['duration'], ax=ax[1], color='salmon');

sns.boxplot(german_df['age'], ax=ax[2], color='darkviolet');

/usr/local/lib/python3.7/dist-packages/seaborn/_decorators.py:43: FutureWarning: Pass the following variable as a keyword arg: x. From version 0.12, the only valid positional argument will be `data`, and passing other arguments without an explicit keyword will result in an error or misinterpretation.

FutureWarning

/usr/local/lib/python3.7/dist-packages/seaborn/_decorators.py:43: FutureWarning: Pass the following variable as a keyword arg: x. From version 0.12, the only valid positional argument will be `data`, and passing other arguments without an explicit keyword will result in an error or misinterpretation.

FutureWarning

/usr/local/lib/python3.7/dist-packages/seaborn/_decorators.py:43: FutureWarning: Pass the following variable as a keyword arg: x. From version 0.12, the only valid positional argument will be `data`, and passing other arguments without an explicit keyword will result in an error or misinterpretation.

FutureWarning

4.2 Relationship between the credit amount and repayment duration

- scatter plot

Observations

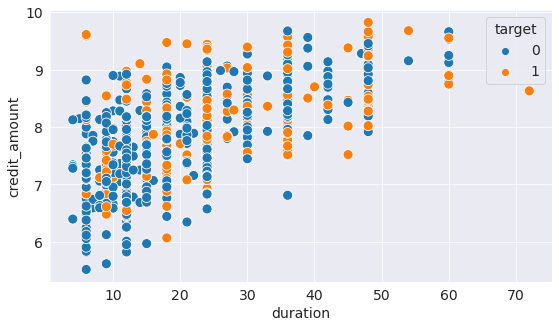

The scatter plot shows that in general, larger loans have longer duration of repayment. Cases where large loans are given with short repayment period have turned out to be bad loans.

sns.scatterplot(y=german_df.credit_amount,

x=german_df.duration,

hue=german_df.target,

s=100,

);

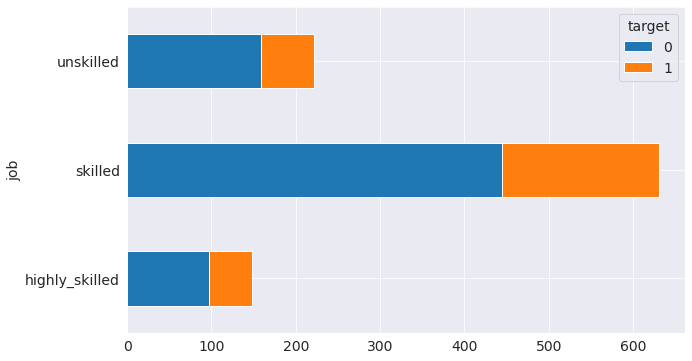

4.3 Exploration of categorical variables

Relationship between credit risk and skills of loan applicant

- Bar-graph

Observations

The graph shows that candidates who are unemployed/unskilled pose a high risk

german_df.groupby('job')['target'].value_counts().unstack(level=1).plot.barh(stacked=True, figsize=(10, 6))

<matplotlib.axes._subplots.AxesSubplot at 0x7effccf2f210>

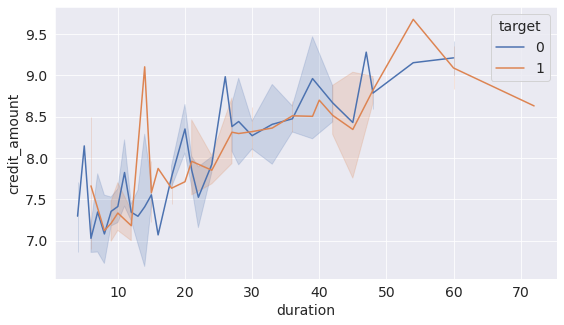

4.4 Relationship between credit amount and duration of the loan

- Line graph

Observation

There is a linear relationship between the credit amount and duration. The larger the credit amount, the longer the repayment duration is.

sns.lineplot(data=german_df, x='duration', y='credit_amount', hue='target', palette='deep');

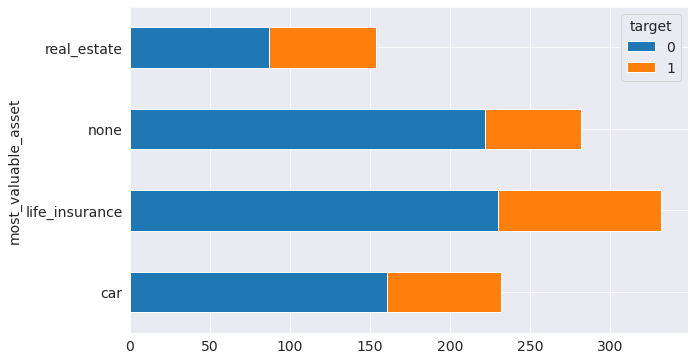

4.5 Relationship between the most valuable asset of the candidate and the credit amount, credit risk

- stacked bar chart

- scatter plot

The categorical coding used in the graphs is:

- A121 : real estate

- A122 : if not A121 : building society savings agreement/life insurance

- A123 : if not A121/A122 : car or other, not in attribute 6

- A124 : unknown / no property

Observations

The graphs show that people with real estate assets are very risky.

german_df.groupby('most_valuable_asset')['target'].value_counts().unstack(level=1).plot.barh(stacked=True, figsize=(10, 6))

<matplotlib.axes._subplots.AxesSubplot at 0x7effcce61d90>

sns.scatterplot(y=german_df.credit_amount,

x=german_df.most_valuable_asset,

hue=german_df.target,

s=100,

);

4. Encode categorical variables

Most machine learning models cannot deal with categorical variables. So, we need to encode the 13 categorical variables that we have in the German dataset.

# Number of unique classes in each object column

german_df.select_dtypes('object').apply(pd.Series.nunique, axis = 0)

account_bal 3

payment_status 5

purpose 10

savings_bond_value 5

employed_since 5

sex_marital 4

guarantor 3

most_valuable_asset 4

concurrent_credits 3

type_of_housing 3

job 3

telephon 2

foreign 2

dtype: int64

We have categorical variables of 2 to 10 categories. We go for Label encoding for variables with only two categories where as for variables with more than two categories, we go for one-hot encoding. In label encoding, we assign each unique category in a categorical variable with an integer. No new columns are created. In one-hot encoding, we create a new column for each unique category in a categorical variable. The only downside to one-hot encoding is that the number of features (dimensions of the data) can explode with categorical variables with many categories. To deal with this, we can perform one-hot encoding followed by PCA or other dimensionality reduction methods to reduce the number of dimensions (while still trying to preserve information).

For label encoding, we use the Scikit-Learn LabelEncoder and for one-hot encoding, the pandas get_dummies(df) function.

# sklearn preprocessing for dealing with categorical variables

from sklearn.preprocessing import LabelEncoder

# Create a label encoder object

le = LabelEncoder()

le_count = 0

# Iterate through the columns

for col in german_df:

if german_df[col].dtype == 'object':

# If 2 or fewer unique categories

if len(list(german_df[col].unique())) <= 2:

# Train on the training data

le.fit(german_df[col])

# Transform both training and testing data

german_df[col] = le.transform(german_df[col])

# Keep track of how many columns were label encoded

le_count += 1

print('%d columns were label encoded.' % le_count)

2 columns were label encoded.

# one-hot encoding of categorical variables

german_df = pd.get_dummies(german_df)

print('Encoded Features shape: ', german_df.shape)

Encoded Features shape: (1000, 58)

Now that we have encoded the variables, let’s continue with the EDA.

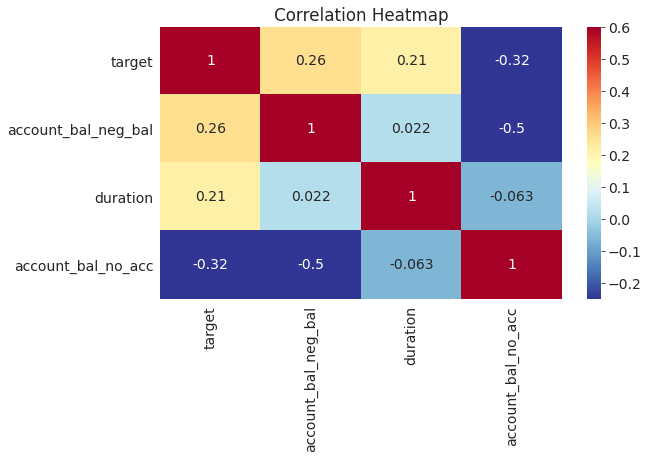

4.1 Correlation between the variables

Let’s look at correlations between the features and the target using Pearson correlation coefficient. In this case, a positive correlation represents correlation with credit default while a negative correlation represents correlation with credit repayment.

Observations:

Positive correlation:

-

People with checking accounts with a negative balance (

account_bal_A11) are likely to default the loan. -

Longer duration loans (

duration) tend to be defaulted.

Negative correlation:

- People with no checking account (

account_bal_A14) are likely to repay the loan.

# Find correlations with the target and sort

correlations = german_df.corr()['target'].sort_values()

# Display correlations

print('Most Positive Correlations:\n', correlations.tail(15))

print('\nMost Negative Correlations:\n', correlations.head(15))

Most Positive Correlations:

sex_marital_A92 0.075493

type_of_housing_A153 0.081556

account_bal_positive_bal 0.089895

type_of_housing_A151 0.092785

concurrent_credits_A141 0.096510

purpose_A40 0.096900

employed_since_A72 0.106397

credit_amount 0.109570

most_valuable_asset_real_estate 0.125750

payment_status_A31 0.134448

payment_status_A30 0.144767

savings_bond_value_A61 0.161007

duration 0.214927

account_bal_neg_bal 0.258333

target 1.000000

Name: target, dtype: float64

Most Negative Correlations:

account_bal_no_acc -0.322436

payment_status_A34 -0.181713

type_of_housing_A152 -0.134589

savings_bond_value_A65 -0.129238

most_valuable_asset_none -0.119300

concurrent_credits_A143 -0.113285

purpose_A43 -0.106922

purpose_A41 -0.099791

age -0.091127

savings_bond_value_A64 -0.085749

foreign -0.082079

sex_marital_A93 -0.080677

employed_since_A74 -0.075980

savings_bond_value_A63 -0.070954

employed_since_A75 -0.059733

Name: target, dtype: float64

Let’s look at the heatmap of significant correlations.

# Extract the significantly correlated variables

corr_data = german_df[['target', 'account_bal_neg_bal','duration','account_bal_no_acc']]

corr_data_corrs = corr_data.corr()

# Heatmap of correlations

sns.heatmap(corr_data_corrs, cmap = plt.cm.RdYlBu_r, vmin = -0.25, annot = True, vmax = 0.6)

plt.title('Correlation Heatmap');

5. Feature engineering

Feature engineering refers to creating most useful features out of the data. This represents one of the patterns in machine learning: feature engineering has a greater return on investment than model building and hyperparameter tuning. [Source]

Feature engineering refers to a general process and can involve both feature construction: adding new features from the existing data, and feature selection: choosing only the most important features or other methods of dimensionality reduction. There are many techniques we can use to both create features and select features.

For this problem, we will try to construct polynomial features.

Polynomial Features

Here, we find interactions between significant features. The correlation between the interaction features and the target is checked. If the interaction features are found to have greater correlation with the target compared to the original features, they are included in the machine learning model as they can help the model learn better.

# Make a new dataframe for polynomial features

poly_features = german_df[['duration','account_bal_neg_bal','account_bal_no_acc']]

poly_target=german_df['target']

from sklearn.preprocessing import PolynomialFeatures

# Create the polynomial object with specified degree

poly_transformer = PolynomialFeatures(degree = 2)

# Train the polynomial features

poly_transformer.fit(poly_features)

# Transform the features

poly_features = poly_transformer.transform(poly_features)

print('Polynomial Features shape: ', poly_features.shape)

Polynomial Features shape: (1000, 10)

This creates a considerable number of new features. To get the names we have to use the polynomial features get_feature_names method.

poly_transformer.get_feature_names(input_features = ['duration','account_bal_neg_bal','account_bal_no_acc'])

['1',

'duration',

'account_bal_neg_bal',

'account_bal_no_acc',

'duration^2',

'duration account_bal_neg_bal',

'duration account_bal_no_acc',

'account_bal_neg_bal^2',

'account_bal_neg_bal account_bal_no_acc',

'account_bal_no_acc^2']

Now, we can see whether any of these new features are correlated with the target.

# Create a dataframe for polynomial features

poly_features = pd.DataFrame(

poly_features, columns = poly_transformer.get_feature_names(

['duration','account_bal_neg_bal','account_bal_no_acc']))

# Add in the target

poly_features['target'] = poly_target

# Find the correlations with the target

poly_corrs = poly_features.corr()['target'].sort_values()

# Display the correlations

poly_corrs

account_bal_no_acc -0.322436

account_bal_no_acc^2 -0.322436

duration account_bal_no_acc -0.232697

duration^2 0.200996

duration 0.214927

account_bal_neg_bal 0.258333

account_bal_neg_bal^2 0.258333

duration account_bal_neg_bal 0.303343

target 1.000000

1 NaN

account_bal_neg_bal account_bal_no_acc NaN

Name: target, dtype: float64

All the new variables have a greater (in terms of absolute magnitude) correlation with the target than the original features. We will add these features to a copy of the German dataset and then evaluate models with and without the features.

list(poly_features)

['1',

'duration',

'account_bal_neg_bal',

'account_bal_no_acc',

'duration^2',

'duration account_bal_neg_bal',

'duration account_bal_no_acc',

'account_bal_neg_bal^2',

'account_bal_neg_bal account_bal_no_acc',

'account_bal_no_acc^2',

'target']

# deleting duplicate columns in poly_features

for i in list(poly_features.columns):

for j in list(german_df.columns):

if (i==j):

poly_features.drop(labels=i, axis=1, inplace=True)

poly_features.drop(labels='1', axis=1, inplace=True)

list(poly_features)

['duration^2',

'duration account_bal_neg_bal',

'duration account_bal_no_acc',

'account_bal_neg_bal^2',

'account_bal_neg_bal account_bal_no_acc',

'account_bal_no_acc^2']

# Print shape of original german_df

print('Original features shape: ', german_df.shape)

# Merge polynomial features into the dataframe

german_df_poly = german_df.merge(poly_features, left_index=True, right_index=True, how = 'left')

# Print out the new shapes

print('Merged polynomial features shape: ', german_df_poly.shape)

Original features shape: (1000, 58)

Merged polynomial features shape: (1000, 64)

german_df_poly.isna().any().any()

False

list(german_df_poly)

['duration',

'credit_amount',

'intallment_rate',

'residence_since',

'age',

'number_of_existcr',

'number_of_dependents',

'telephon',

'foreign',

'target',

'account_bal_neg_bal',

'account_bal_no_acc',

'account_bal_positive_bal',

'payment_status_A30',

'payment_status_A31',

'payment_status_A32',

'payment_status_A33',

'payment_status_A34',

'purpose_A40',

'purpose_A41',

'purpose_A410',

'purpose_A42',

'purpose_A43',

'purpose_A44',

'purpose_A45',

'purpose_A46',

'purpose_A48',

'purpose_A49',

'savings_bond_value_A61',

'savings_bond_value_A62',

'savings_bond_value_A63',

'savings_bond_value_A64',

'savings_bond_value_A65',

'employed_since_A71',

'employed_since_A72',

'employed_since_A73',

'employed_since_A74',

'employed_since_A75',

'sex_marital_A91',

'sex_marital_A92',

'sex_marital_A93',

'sex_marital_A94',

'guarantor_A101',

'guarantor_A102',

'guarantor_A103',

'most_valuable_asset_car',

'most_valuable_asset_life_insurance',

'most_valuable_asset_none',

'most_valuable_asset_real_estate',

'concurrent_credits_A141',

'concurrent_credits_A142',

'concurrent_credits_A143',

'type_of_housing_A151',

'type_of_housing_A152',

'type_of_housing_A153',

'job_highly_skilled',

'job_skilled',

'job_unskilled',

'duration^2',

'duration account_bal_neg_bal',

'duration account_bal_no_acc',

'account_bal_neg_bal^2',

'account_bal_neg_bal account_bal_no_acc',

'account_bal_no_acc^2']

6. Data split to train and test datasets

As the German dataset is an imbalanced dataset with more number repayors compared to defaulters, we used stratified random test_train_split to split the dataset into random test and train datasets so that relative class frequencies are preserved.

from sklearn.model_selection import train_test_split

x, y = german_df.drop('target', axis=1), german_df['target']

x.shape, y.shape

((1000, 57), (1000,))

x_train, x_test, y_train, y_test= train_test_split(x,y, test_size=.2, random_state=42, stratify=y)

x_train.shape, x_test.shape

((800, 57), (200, 57))

x_train

y_train

828 1

997 0

148 0

735 0

130 0

..

492 0

545 1

298 0

417 0

749 0

Name: target, Length: 800, dtype: int64

# train and test split on german_df_poly

X, Y = german_df_poly.drop('target', axis=1), german_df_poly['target']

print(X.shape, Y.shape)

X_train, X_test, Y_train, Y_test= train_test_split(X,Y, test_size=.2, random_state=42, stratify=Y)

(1000, 63) (1000,)

7. Models

Evaluation criteria

Let’s have a look at the different options available.

| Evaluation criteria | Description |

|---|---|

| Accuracy | (true positive+ true negative) / total obs |

| Precision | true positive/ total predicted positive |

| Recall | true positive/ total actual positive |

| F1 | 2* precision * recall / (precision + recall) |

| AUC ROC | Area Under ROC Curve (TPR Vs. FPR for all classification thresholds) |

-

Accuracy: The German dataset is an imbalanced dataset. Accuracy would give a high score by predicting the majority class but would fail to predict the minority class, which is the defaulters. Hence, this is not a suitable metric for this dataset.

-

Precision: Precision is a good metric when the costs of false positive are high. Example, email spam detection.

-

Recall: This metric is suitable when the costs of false negative are high. Example, predicting a defaulter as not defaulter. This costs a huge loss for the bank. Hence, this is a suitable metric for our case.

-

F1: measure of both precision and recall.

- AUC ROC: It is the plot of TPR vs FPR. All other criteria discussed here assume 0.5 as the decision threshold for the classification. However, it may not be always true. The AUC helps us evaluate the performance of the model for all classification thresholds. The higher the value of the AUC metric, the better the model.

- True positive rate (TPR) = TP/ Total actual positive

- False positive rate (FPR) = FP/ Total actual negative

We will use Recall and AUC ROC as evaluation metric.

Baseline

y.value_counts(normalize=True)

0 0.7

1 0.3

Name: target, dtype: float64

It means that the baseline accuracy is 70%, i.e., even if we classify all the samples as defaulters, we will be 70% accurate.

Models without tuning

# import packages, functions, and classes

from sklearn.ensemble import RandomForestClassifier

from sklearn.linear_model import LogisticRegression

from sklearn.tree import DecisionTreeClassifier

from sklearn.neighbors import KNeighborsClassifier

from xgboost import XGBClassifier

from sklearn.metrics import roc_auc_score, recall_score, classification_report

from sklearn.model_selection import StratifiedKFold, cross_val_score, cross_validate

# prepare models

models = []

models.append(('DT', DecisionTreeClassifier(random_state=42)))

models.append(('LR', LogisticRegression(random_state=42)))

models.append(('RF', RandomForestClassifier(random_state=42)))

models.append(('XGB', XGBClassifier(random_state=42)))

models.append(('KNN', KNeighborsClassifier()))

# evaluate each model in turn

results_recall = []

results_roc_auc= []

names = []

# recall= tp/ (tp+fn). Best value=1, worst value=0

scoring = ['recall', 'roc_auc']

for name, model in models:

# split dataset into k folds. use one-fold for validation and remaining k-1 folds for training

skf= StratifiedKFold(n_splits=10, shuffle=True, random_state=42)

# Evaluate a score by cross-validation. Returns array of scores of the model for each run of the cross validation.

#cv_results = cross_val_score(model, x_train, y_train, cv=skf, scoring=scoring)

cv_results = cross_validate(model, x_train, y_train, cv=skf, scoring=scoring)

results_recall.append(cv_results['test_recall'])

results_roc_auc.append(cv_results['test_roc_auc'])

names.append(name)

msg = "%s- recall:%f roc_auc:%f" % (name, cv_results['test_recall'].mean(),cv_results['test_roc_auc'].mean())

print(msg)

# boxplot algorithm comparison

#recall score plots

fig = plt.figure(figsize=(11,6))

fig.suptitle('Recall scoring Comparison')

ax = fig.add_subplot(111)

plt.boxplot(results_recall, showmeans=True)

ax.set_xticklabels(names)

plt.show();

# roc auc score box plots

fig = plt.figure(figsize=(11,6))

fig.suptitle('AUC scoring Comparison')

ax = fig.add_subplot(111)

plt.boxplot(results_roc_auc, showmeans=True)

ax.set_xticklabels(names)

plt.show();

Gaussian NB model has the highest roc_auc score. However, Logistic regression, Randon forests and XGBoost has a better AUC score than Gaussian NB. Now let us tune hyperparameters for each of these models.

from sklearn.metrics import accuracy_score, confusion_matrix, roc_auc_score, recall_score

from sklearn.model_selection import StratifiedKFold, cross_val_score

from sklearn.model_selection import GridSearchCV

7.2 Logistic regression

- first, fit on the original dataset set. Then, fit on polynomial features obtained by feature engineering

-

polynomial features gives better results. Hence, this dataset will be used for further exploration

- C: variable that controls regularization. Smaller values indicate higher regularization. It’s a penalty term that disincentivize overfitting

First let us choose between german_df and german_df_poly. Use C=0.0001 which is randomly chosen.

# Logistic model on data=german_df

log_reg = LogisticRegression(C = 0.0001, random_state=42)

log_reg.fit(x_train, y_train)

print('Dataset: german_df\n Recall score on train set: {:.2f}'.format(cross_val_score(log_reg, x_train, y_train, cv=skf, scoring='recall').mean()))

# Logistic model on data=german_df_poly

log_reg_poly = LogisticRegression(C = 0.0001, random_state=42, solver='lbfgs', max_iter=1000)

log_reg_poly.fit(X_train, Y_train)

print('Dataset: german_df_poly\n Recall score on train set: {:.2f}'.format(cross_val_score(log_reg_poly, X_train, Y_train, cv=skf, scoring='recall').mean()))

Dataset: german_df

Recall score on train set: 0.01

Dataset: german_df_poly

Recall score on train set: 0.18

We see considerable improvement in recall score with german_df_poly dataset. Hence, we proceed with german_df_poly for tuning regularization parameter C.

C=[1,0.1,0.01,0.001,0.0001]

# Create lists to save the values of recall score on training and test sets

train_recall = []

test_recall = []

for c in C:

log_reg_poly = LogisticRegression(C = c, random_state=42, solver='lbfgs', max_iter=5000).fit(X_train, Y_train)

train_recall.append(cross_val_score(log_reg_poly, X_test, Y_test, cv=skf,scoring='recall').mean())

test_recall.append(recall_score(Y_test, log_reg_poly.predict(X_test)))

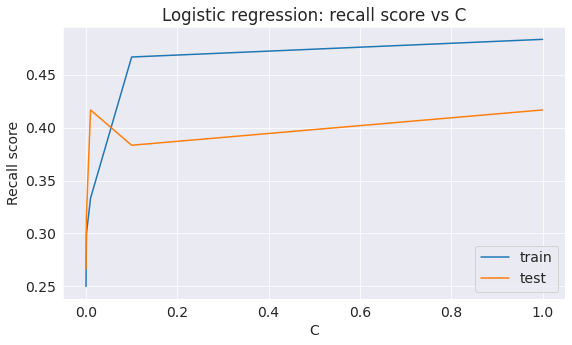

# plot graph of recall score vs. C

plt.plot(C, train_recall, label='train')

plt.plot(C, test_recall, label='test')

plt.legend()

plt.xlabel('C')

plt.ylabel('Recall score')

plt.title('Logistic regression: recall score vs C');

test_recall

[0.4166666666666667,

0.38333333333333336,

0.4166666666666667,

0.31666666666666665,

0.26666666666666666]

We get the maximum recall score on test set with overfitting at C=0.01

# Final logistic model

log_reg_poly = LogisticRegression(C = 0.01, random_state=42, solver='lbfgs', max_iter=5000).fit(X_train, Y_train)

print('Recall score on test dataset: {:.2f}'.format(recall_score(Y_test, log_reg_poly.predict(X_test))))

print('\nAUC ROC score on test dataset: {:.2f}'.format(roc_auc_score(Y_test,log_reg_poly.predict_proba(X_test)[:, 1])))

Recall score on test dataset: 0.42

AUC ROC score on test dataset: 0.78

7.3 Random Forest

- find optimal number of trees

- max depth

- min number of samples per leaf

- max features

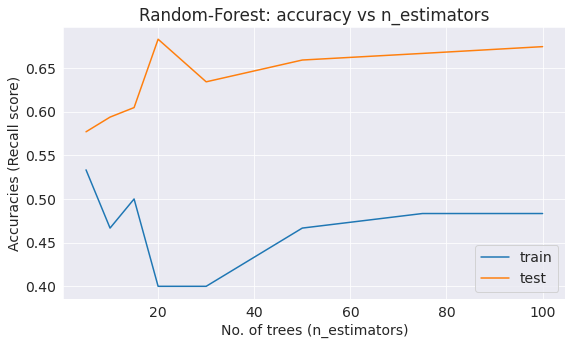

Now, let’s try to improve this result. Let’s start with the number of trees.

# Create lists to save the values of accuracy on training and test sets

train_acc = []

test_acc = []

trees_grid = [5, 10, 15, 20, 30, 50, 75, 100]

for ntrees in trees_grid:

rf = RandomForestClassifier(n_estimators=ntrees, random_state=42, n_jobs=-1).fit(X_train, Y_train)

train_acc.append(cross_val_score(rf, X_train, Y_train, cv=skf, scoring='recall').mean())

test_acc.append(recall_score(rf.predict(X_test), Y_test))

print("Best recall score on test dataset is {:.2f}% with {} trees".format(max(test_acc)*100,

trees_grid[np.argmax(test_acc)]))

# plot

plt.plot(trees_grid, train_acc, label='train')

plt.plot(trees_grid, test_acc, label='test')

plt.legend()

plt.xlabel('No. of trees (n_estimators)')

plt.ylabel('Accuracies (Recall score)')

plt.title('Random-Forest: accuracy vs n_estimators');

Best recall score on test dataset is 68.29% with 20 trees

Best accuracy is achieved with 20 tress.

# Initialize the set of parameters for exhaustive search and fit

parameters = {'max_features': [7, 10, 16, 18],

'min_samples_leaf': [1, 3, 5, 7],

'max_depth': [15, 20, 24, 27]}

rf = RandomForestClassifier(n_estimators=20, random_state=42, n_jobs=-1)

gcv = GridSearchCV(rf, parameters, n_jobs=-1, cv=skf, verbose=1, scoring='recall')

gcv_fit= gcv.fit(X_train, Y_train)

Fitting 10 folds for each of 64 candidates, totaling 640 fits

[Parallel(n_jobs=-1)]: Using backend LokyBackend with 2 concurrent workers.

[Parallel(n_jobs=-1)]: Done 46 tasks | elapsed: 5.5s

[Parallel(n_jobs=-1)]: Done 196 tasks | elapsed: 22.1s

[Parallel(n_jobs=-1)]: Done 446 tasks | elapsed: 49.8s

[Parallel(n_jobs=-1)]: Done 640 out of 640 | elapsed: 1.2min finished

# evaluate on train and test datasets

cross_val= cross_val_score(gcv_fit.best_estimator_, X_train, Y_train, cv=skf,scoring='recall').mean()

recall_sc=recall_score(Y_test,gcv_fit.best_estimator_.predict(X_test))

roc_sc= roc_auc_score(Y_test,gcv_fit.best_estimator_.predict_proba(X_test)[:, 1])

# print scores

print("GCV best parameters: ",gcv.best_params_)

print("GCV best score: {:.2f}".format(gcv.best_score_))

print("Cross val score on train dataset: {:.2f}".format(cross_val))

print("Recall score on test dataset: {:.2f}".format(recall_sc))

print("ROC AUC score on test dataset: {:.2f}".format(roc_sc))

GCV best parameters: {'max_depth': 20, 'max_features': 18, 'min_samples_leaf': 3}

GCV best score: 0.48

Cross val score on train dataset: 0.48

Recall score on test dataset: 0.40

ROC AUC score on test dataset: 0.74

7.4 XGBoost

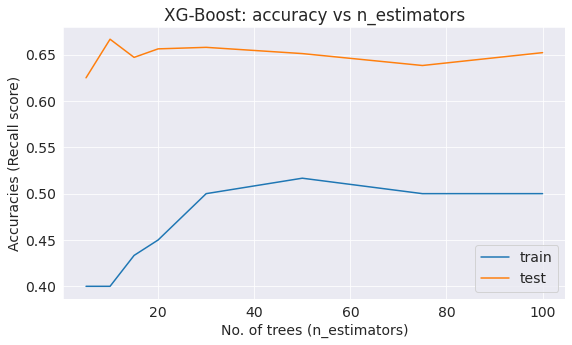

# Create lists to save the values of accuracy on training and test sets

train_acc = []

test_acc = []

estimator_grid = [5, 10, 15, 20, 30, 50, 75, 100]

for nestimator in estimator_grid:

xg = XGBClassifier(n_estimators=nestimator, random_state=42, n_jobs=-1).fit(X_train, Y_train)

train_acc.append(cross_val_score(xg, X_test, Y_test, cv=skf, scoring='recall').mean())

test_acc.append(recall_score(xg.predict(X_test), Y_test))

print("Best recall score on test dataset is {:.2f}% with {} estimators".format(max(test_acc)*100,

estimator_grid[np.argmax(test_acc)]))

# plot

plt.plot(estimator_grid, train_acc, label='train')

plt.plot(estimator_grid, test_acc, label='test')

plt.legend()

plt.xlabel('No. of trees (n_estimators)')

plt.ylabel('Accuracies (Recall score)')

plt.title('XG-Boost: accuracy vs n_estimators');

Best recall score on test dataset is 66.67% with 10 estimators

#model

model_xg = XGBClassifier(random_state=42)

model_xg.fit(X_train, Y_train)

#evaluate

print('Train accuracy:', cross_val_score(model_xg, X_train, Y_train, cv=skf, scoring='recall').mean())

print('Recall score on test dataset:', recall_score(Y_test, model_xg.predict(X_test)))

print('ROC AUC score on test dataset:', roc_auc_score(Y_test, model_xg.predict_proba(X_test)[:,1]))

Train accuracy: 0.45

Recall score on test dataset: 0.5

ROC AUC score on test dataset: 0.7957142857142858

# Initialize the set of parameters for exhaustive search and fit

parameters = {'max_features': [7, 10, 16, 18],

'min_samples_leaf': [1, 3, 5, 7],

'max_depth': [15, 20, 24, 27]}

model_xg = XGBClassifier(n_estimators=10, random_state=42, n_jobs=-1)

gcv = GridSearchCV(model_xg, parameters, n_jobs=-1, cv=skf, verbose=1, scoring='recall')

gcv_fit= gcv.fit(X_train, Y_train)

Fitting 10 folds for each of 64 candidates, totaling 640 fits

[Parallel(n_jobs=-1)]: Using backend LokyBackend with 2 concurrent workers.

[Parallel(n_jobs=-1)]: Done 88 tasks | elapsed: 4.6s

[Parallel(n_jobs=-1)]: Done 388 tasks | elapsed: 20.1s

[Parallel(n_jobs=-1)]: Done 640 out of 640 | elapsed: 33.0s finished

gcv.best_params_, gcv.best_score_

({'max_depth': 15, 'max_features': 7, 'min_samples_leaf': 1}, 0.4625)

# evaluate on train and test datasets

cross_val= cross_val_score(gcv_fit.best_estimator_, X_train, Y_train, cv=skf,scoring='recall').mean()

recall_sc=recall_score(Y_test,gcv_fit.best_estimator_.predict(X_test))

roc_sc= roc_auc_score(Y_test,gcv_fit.best_estimator_.predict_proba(X_test)[:, 1])

# print scores

print("GCV best parameters: ",gcv.best_params_)

print("GCV best score: {:.2f}".format(gcv.best_score_))

print("Cross val score on train dataset: {:.2f}".format(cross_val))

print("Recall score on test dataset: {:.2f}".format(recall_sc))

print("ROC AUC score on test dataset: {:.2f}".format(roc_sc))

GCV best parameters: {'max_depth': 15, 'max_features': 7, 'min_samples_leaf': 1}

GCV best score: 0.46

Cross val score on train dataset: 0.46

Recall score on test dataset: 0.43

ROC AUC score on test dataset: 0.73

7.5 KNN

from sklearn.neighbors import KNeighborsClassifier

knn= KNeighborsClassifier(n_neighbors = 1)

knn.fit(X_train, Y_train)

#evaluate

print('Train accuracy:{:.2f}'.format(cross_val_score(knn, X_train, Y_train, cv=skf, scoring='recall').mean()))

print('Recall score on test dataset:{:.2f}'.format(recall_score(Y_test, knn.predict(X_test))))

print("ROC AUC score on test dataset: {:.2f}".format(roc_auc_score(Y_test,gcv_fit.best_estimator_.predict_proba(X_test)[:, 1])))

Train accuracy:0.49

Recall score on test dataset:0.35

ROC AUC score on test dataset: 0.73

Model evaluation

| MODEL | Recall score on test data | ROC AUC score on test data |

|---|---|---|

| Logistic Regression | 0.42 | 0.78 |

| Random Forest | 0.40 | 0.74 |

| XGBoost | 0.43 | 0.73 |

| KNN | 0.35 | 0.75 |

Conclusion

Recall, also known as sensitivity, is calculated as True Positives / Total Actual Positives, or TP / (TP + FN). A perfect recall score is 1, which occurs when there are no false negatives (FN = 0). In the context of a credit risk prediction model, our goal is to correctly identify all defaulters. Therefore, we prioritize models with the highest recall. In this case, the XGBoost model achieves the highest recall score and is thus the preferred choice.

References and Future Work

Machine learning can be used on this dataset to develop a model that can predict bad loans. This might require the use of classifiers.

References:

- Jovian Zero to Pandas course (https://jovian.ai/learn/data-analysis-with-python-zero-to-pandas)

- https://seaborn.pydata.org

- https://pandas.pydata.org

- MLCourse.ai (https://mlcourse.ai/lectures)

- Accuracy, precision, recall, or F1 by Koo Ping Shung (https://towardsdatascience.com/accuracy-precision-recall-or-f1-331fb37c5cb9)